Bitcoin is digital currency that uses peer-to-peer technology to enable instant payments to anyone. It uses open source software called Bitcoin Core to enable the use of the currency.

Every once in a while, a new idea is bornone that has the potential to question the very foundations of everything we know about the world as it is today. The ideas I am talking about are those that have changed and will change the world for the better. Take email, for example at its inception, people thought it was for the geeks and wouldnt catch on. I would have agreed in the early days, but look at how the world has become so dependent on it over the last few decades. This is an ongoing phenomenonwhat is old will either perish or evolve. The only constant, if any, is change.

On a cold winter morning of January 2009, Satoshi Nakamoto set out to change the way we transact business and unleashed the worlds first cryptocurrency, bitcoin.

A cryptocurrency is a form of digital currency that uses cryptography (the science of hiding messages in codes that appear to be a random string of characters) as a means of generating new units and securing transactions. Its heavy dependence on cryptography is how it derived its name.

Though Bitcoin is by far the most popular cryptocurrency, a few others like Litecoin and Ripple are also gaining momentum.

The history of Bitcoin

In 2008, Satoshi Nakamoto, founder of Bitcoin, published a paper titled Bitcoin: A Peer-to-Peer Electronic Cash System (http://goo.gl/MqyCW7), which explained in detail how a peer-to-peer (P2P) currency would work. In January 2009, he officially launched the Bitcoin network. Complementing that, he also launched the Bitcoin Core software (http://goo.gl/gUbUq), which would help people mine (a term explained later) and trade (please refer to An Introduction to Bitcoin: The Open Source Cryptographic Currency, published in the November 2013 edition of Open Source For You) in bitcoins. The Bitcoin Project was released under the MIT licence, which essentially meant that its free and open source. The new currency rapidly gained momentum and became the talk of the town. It proved to be a nightmare for banks and governments worldwide but it became the darling of the online underworld (for reasons that I will go into later).

After launching Bitcoin, Satoshi Nakamoto gradually disappeared from the online world leaving his creation in the hands of the community, which was by then swearing by it. Surprisingly, in this well-connected and spied-upon world, Nakamoto still remains a mysterious figure. While many have speculated about who he really is, no one has arrived at any conclusive proof about his identity. Given the complexity and sophistication of the Bitcoin system, many researchers believe that it cant be the work of a single person. They believe that some kind of group or consortium of technology companies is behind this cryptocurrency. Considering that Bitcoin mining is processing power-intensive, these companies would surely stand to benefit from selling the concept to the Bitcoin community.

What is a bitcoin?

Given its name and logo, people mistakenly assume that it is a physical coin with electromagnetic capabilities, which is contrary to the very notion of a cryptocurrency. The essence of a cryptocurrency is that it is not required to and cannot exist in a physical form.

The following analogy will help you understand the concept of Bitcoin better. Lets say you have 10,000 units of a currency in a bank account and you can conduct online transactions with this account. At any given moment, the amount of currency available to you for conducting transactions is the cumulative sum of all the transactions youve performed till date via that account. Now, as long as you dont withdraw the amount physically, its just a number stored in the banks database. When you perform an online transaction, using this account, it is recorded in your account the relevant number is either deducted from your account or credited to it, depending on the nature of your transaction. Again, as long as you dont withdraw the balance amount physically, it exists in a virtual state in the banks database. This is what bitcoin is, except that with bitcoins, you are your own bank; your bitcoin wallet is your bank account and you cant withdraw it physically. You can exchange it in return for some other currency but you cant have bitcoins in physical form because they only exist in digital (or virtual) form.

Thou shalt remain in states of 0s and 1s forever

Hey! Hold on

I have to first deposit 10,000 units of hard cash with the bank before they can become virtual and here youre saying that bitcoin only exists in virtual from. How does this work? Where are all these bitcoins coming from?

Bitcoins originate via a process called bitcoin mining. Before I delve more into it, lets understand how the Bitcoin network works and how a transaction takes place. As I mentioned earlier, Bitcoin is a peer-to-peer network, which means that theres no single entity controlling it. It is a decentralised network and each system in this network acts as a node.

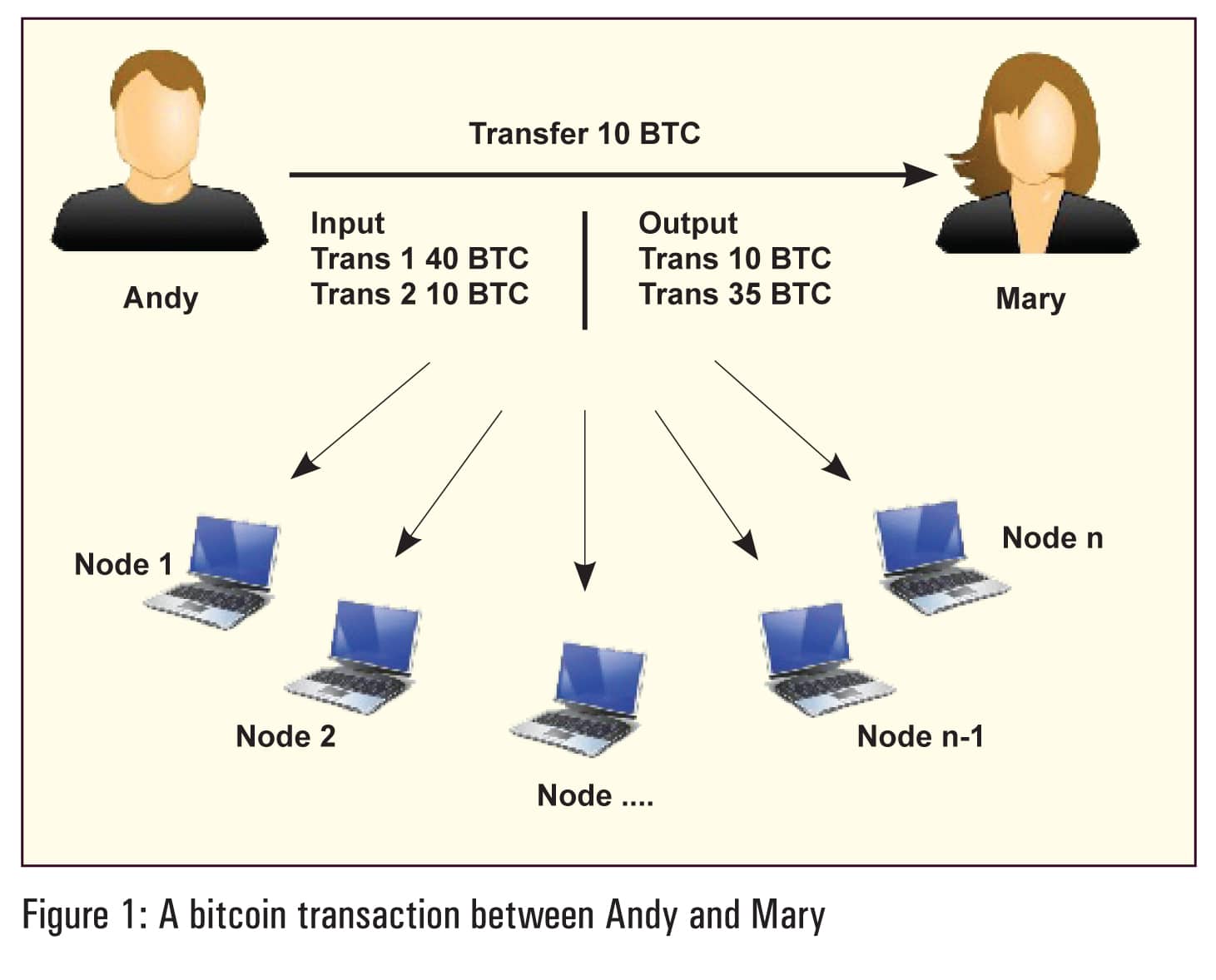

Lets assume that Andy and Mary are conducting a transaction in bitcoin (BTC), in which Andy wants to transfer 10 BTC to Mary in return for a service and he currently has a total of 50 BTC in his bitcoin wallet. Figure 1 depicts how the transaction between them would look.

There are two parts to this transactionthe input and output. The input part contains a reference to the previous transactions, which would account for the amount of BTC currently in Andys wallet. The output part will contain the information of how many bitcoins Andy wants to transfer (10 BTC in this case) and how much change he wants back (35 BTC in this case). The difference between the amount he wants to transfer and the change he wants back, if any, is the transaction fee (5 BTC in this case). The transaction fee is the incentive for bitcoin miners to include that transaction in a transaction block (explained later). Andy will then sign this transaction with his digital signature and publish it to the Bitcoin network. All nodes in the Bitcoin network will receive this transaction. They may or may not act upon it, depending on their role in the network.

A bitcoin miner is a node in the Bitcoin network, running bitcoin mining software. A bitcoin mining node collects Andys transaction, along with many others, and collates them into what is called a transaction block. If this block is accepted by the network, it will then be appended to the universal transaction block chain. Think of the transaction block chain as a universal ledger which has all the transactions recorded in it, since the beginning of the Bitcoin system. Once the miners transaction blocks are accepted, they are rewarded with a certain number of bitcoins (in addition to the transaction fee) that accrues from all the transactions included in that block. This reward part is how new bitcoins are created in the Bitcoin network.

On the face of it, the bitcoin mining process might seem to be a very simplistic process, but it actually involves its share of complexity. The Bitcoin network doesnt simply accept a transaction blocka miner has to prove the effort he has put in while working on that transaction block. This is called proof of work.

Proof of work is a cryptographic puzzle, which the Bitcoin network requires the miner to solve before the transaction block is accepted within the transaction block chain. The creation of a transaction block is fairly simple and doesnt require much effort; solving this puzzle is what makes mining a processing power-intensive task. The difficulty level of the puzzle is decided by the Bitcoin network, which is designed to adjust it, depending on how fast transaction blocks are being generated. If it senses that blocks are being generated too fast, the network increases the difficulty level and vice versa. The miner who solves the proof of work puzzle first, publishes the solution on the network. The Bitcoin network then verifies the solution sent by the miner, and if correct, the transaction block is appended to the transaction block chain. Though generating the solution is processing power-intensive, verifying it hardly takes any time.

While mining is one way in which bitcoins circulate, there are three much simpler ways:

- Exchanging bitcoins in return for some other currency, either from a designated exchange or from a person willing to make such an exchange. Its 100 per cent legal, as of date, though the Reserve Bank of India advises against it (http://goo.gl/fbh3wO).

- Accepting bitcoins for a service or product.

- Asking a friend for some (this might be bit tricky, given the current value of the bitcoin).

Note: Mining is the only method by which new bitcoins are created. The three above-mentioned methods simply help in circulating them.

What about securing this currency?

Hmm

so how secure is it? With other currencies, Ive got banks and their robust systems protecting my money, but this sounds like its all on me.

Well, thats both true and false. With bitcoins, youll need to be a bit more careful but such is the case with banks too. If youre casual in handling your bank account numbers and passwords, there is a fairly high risk of you losing your money even from your supposedly safe bank account.

Besides, the foundation of Bitcoin is laid using one of the principle elements of information security, which is cryptography. Unless somebody invents a supercomputer that can break the sophisticated algorithms at play in the Bitcoin network (some agencies are trying hard but even they havent achieved any significant progress on this front yet), theres only a very small likelihood of the network getting breached.

This brings us to the second most common concern when dealing with currencyfraud. There have been very few successful attempts to fraud the Bitcoin network but even those didnt last long. Security researchers have tried to break in but they couldnt (http://goo.gl/fSlsMZ).

Still, lets assume that somebody does give it a shot. Since the sanctity of the Bitcoin network is dependent on the transaction block chain, the most common way to fraud the system would be to introduce malicious transactions in the chain. Carrying forward the earlier-mentioned example, lets assume that Andy has malicious intentions and he wants to cheat Mary. Right after his transaction with her, he creates another transaction in which he transfers the 10 BTC back to himself.

On an average, every 10 minutes a transaction block is added to the transaction block chain and once this is added, the miners stop working with the previous block and start on the one thats just added. At any given moment, there are thousands of miners putting together their processing power simultaneously to honestly mine bitcoins.

If Andy wants to introduce the malicious transaction in the chain, he has to create a new transaction block with that transaction in it, and challenge not only the transaction block in which his first transaction was but also all the ones added after that. The challenge for Andy is to solve the proof of work puzzle for the block that has the genuine transaction and for each block in the chain, after that particular one. This boils down to the processing power available with him, competing with the processing power available with thousands of honest bitcoin miners. Unless Andy has resources to obtain that kind of processing power and a much bigger incentive than his investment, hes not going to make it.

The fraud that Andy was trying to commit in the above example is called double-spending, i.e., spending exactly the same money twice. In the banking system, banks and payment gateways usually monitor systems for double-spending. In the Bitcoin network, the network itself takes care of it, as long as the processing power of honest miners is more than that of a fraudster.

The Bitcoin network has another security enhancement that beats the current banking system, and that is anonymity. Similar to the banking system, in the Bitcoin network too your wallet is represented by a string of seemingly random characters but thats all they have in common on this front. The Bitcoin network doesnt need to know who you are, nor your address, age and other detailsall of which are required by the banking system.

The pros and cons

Ive heard you out. But I am still sceptical

Like every other thing out there, bitcoins also ship with a list of pros and cons.

The pros:

- The Bitcoin network is decentralised, which means no single authority, bank or government can control or regulate it. Therefore, it is inflation-proof.

- Theres no third party involved while transacting in bitcoins. Its all person-to-person.

- Even though the transactions are public, it provides complete anonymity. People can know how much balance a particular account has but they cant find out who owns that account.

- There are no bank fees, credit card charges, service charges, etc. A bitcoin can be transferred from one account to another at the click of a key, irrespective of the country, state or city.

- The transactions done in bitcoins are irreversible and thereby prevent merchants from fraud purchases.

- Anyone with an Internet connection can deal in bitcoins.

The cons:

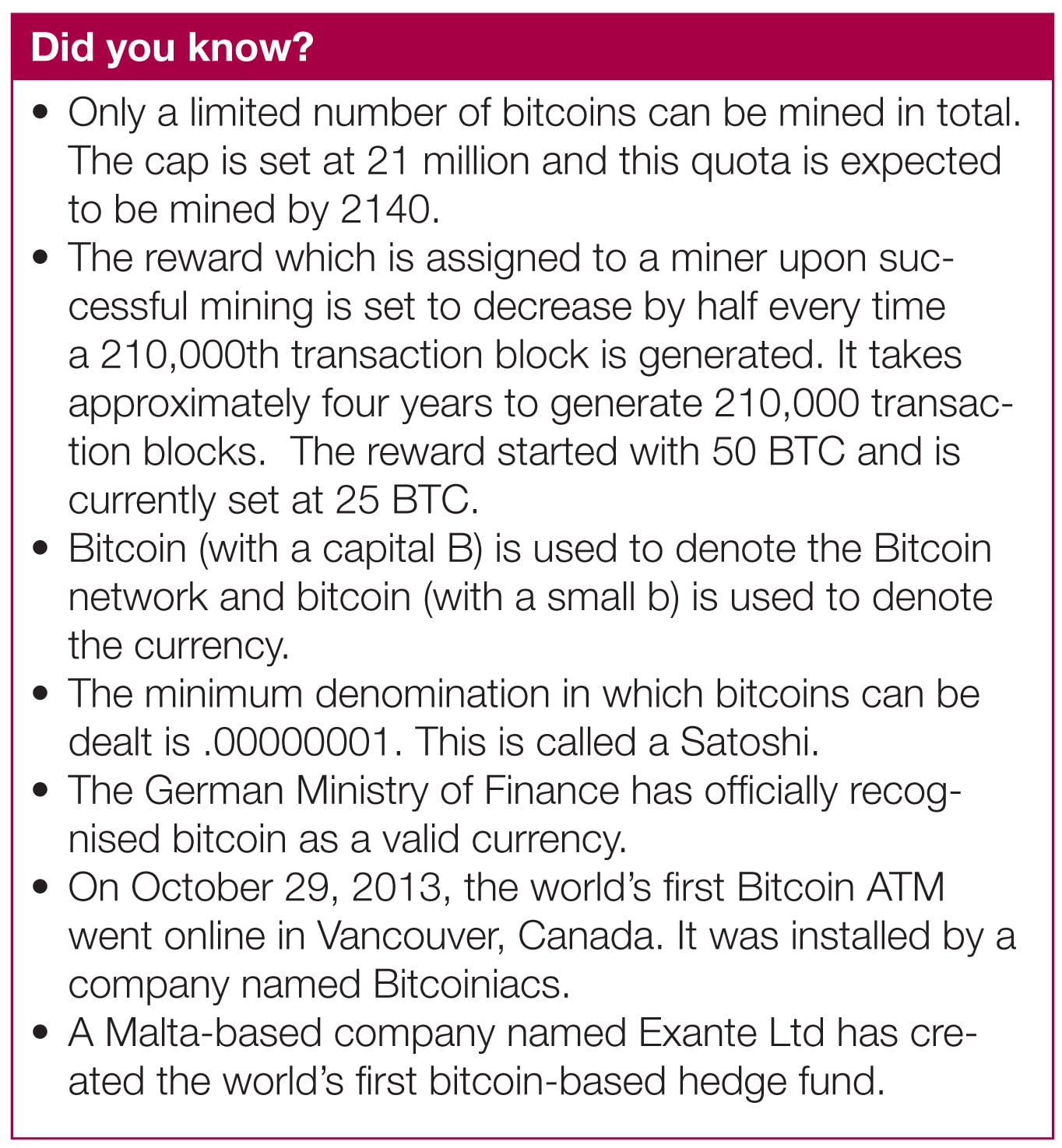

- The network is highly volatile. Unless youre a miner, youll have to buy bitcoins with alternate currency. The exchange rate of a bitcoin is purely governed by demand and supply. When it started out, the exchange rate was US$ .0008 per BTC and achieved a maximum rate of $1100 per BTC in November 2013 (http://goo.gl/pqQ7L).

- There is a potential for the bitcoin to lose value if a better cryptocurrency crops up.

Its irrecoverable. Unfortunately, if you lose access to your bitcoin wallet, theres no way to get it back. Youll have to write it off. - Governments are staying away from it.

What you might be wondering

- Can the governments completely ban Bitcoin?

As mentioned earlier, bitcoins are not issued by any government, so they literally have no say in how its circulated. This also means that they cannot completely ban bitcoins. However, they can make dealing in it illegal. But even then, theres no way for the state to track whos dealing in bitcoins because of the anonymity it provides. Besides, even if some countries ban it, not all governments will share the same viewpoint. - Why are governments and banks sceptical of Bitcoin?

Why does anybody fear anything? Either they dont understand it or are threatened by it. I am sure we can cross off the former reason. Governments and banks are feeling threatened because they have genuine reason to be. Bitcoin is questioning the way currency and banks work and the latter dont know how its going to turn out. They can speculate for sure, but nothing is certain. In simple words, governments and banks are afraid to lose control. - People believe it to be a Ponzi scheme. Are they right?

The main principle at work in any Ponzi scheme is that theres a single entity behind it. This entity has malicious intentions and at an opportune moment, runs away with the money. With Bitcoin, theres no single entity controlling it. All the work is done by nodes and miners. There might have been a possibility of a backdoor in the software code, but its open source! Any such bug, flaw or backdoor would be visible to the community and will be fixed before any harm can be caused. - Is it possible to take down the Bitcoin network?

Yes, if the community loses faith in it, it may decide not to be a part of the network. However, itll be a very difficult task for any government or national agency to take down the network because it has spread across the world. Its very similar to the BitTorrent network. Even if they do take it down, the source code is available to anyone. A similar network can be created by anyone, anywhere in the world. - Is it safe to invest in bitcoin?

Personally, I would advise against it. However, if you wish to experiment, either wait till the exchange rate drops or ask a friend.

A more exhaustive list of frequently asked questions about Bitcoin is available at http://goo.gl/x1Tm7m.

Satoshi Nakamoto has started a revolution in the form of Bitcoin which, if successful, holds the potential to replace the concept of currencies as we know it. More and more people are seeing value in dealing in bitcoins. Today, you can buy a beer, pizza, groceries, etc, by paying in bitcoins. Going by the current trend, it would seem that Bitcoin is here to stay.

{kind=link}