Blockchain technology has gained significant attention within a short span of time, and is predicted to grow exponentially and revolutionise the current financial ecosystem. This article takes a quick look at the foundational concepts of blockchain technology.

In the existing financial setup, banks and governments act as intermediaries for any electronic payment (by an individual or business), creating trust and certainty by facilitating the transaction of goods and services. However, they often cause delays and impede the free flow of business due to the time it takes to process transactions and meet regulatory requirements. And even a system managed by a central governing authority is prone to being hacked or corrupted.

Therefore, there is need for a technology that enables direct business-to-business (B2B) or peer-to-peer transactions without the involvement of any banks, government or intermediary third parties. In 2008, blockchain technology was invented by Satoshi Nakamoto (a pseudonym for a person or group) to address these issues. This technology creates a decentralised digital public record of transactions, which is secure, anonymous, tamper-proof and unchangeable. In this technology, the block is a part of a blockchain, which is a combination of three items — a hash pointer to the previous block, a timestamp, and transaction data such as the sender, receiver and number of Bitcoins.

Benefits of blockchain compared to banks or other intermediary systems

- Unlike intermediary systems that maintain private databases of records, a blockchain makes all records public with increased transparency.

- Blockchain technology eliminates expensive intermediary fees, thereby removing a substantial burden on individuals and businesses.

- Hacking attacks and fraudulent activities that typically impact large central intermediaries are not possible with blockchain technology.

Therefore, security and transparency are the two main features and advantages of blockchain technology. And the fact that a blockchain is immutable, makes tampering with information practically impossible.

Role of cryptocurrency in blockchain

Cryptocurrency is a combination of cryptography and currency. It is digital currency that uses encryption techniques to regulate the generation of monetary units and verify the transfer of funds, independent of any central authority. These currencies are not issued by a central government and are used to facilitate the transfer of funds between two parties.

Bitcoin, Litecoin, Ripple, Ethereum and Zcash are the popular cryptocurrencies currently. Among these, Bitcoin is the world’s foremost, invented by the same person (or group) Satoshi Nakamoto in 2009. One of the leading official sites that monitors the trading of digital cryptocurrencies is CoinCap.

Understanding Bitcoin mining

Mining is the verification of bitcoin transactions. As shown in Figure 1, let us suppose Hema wants to buy a computer from David, using Bitcoin. To make sure her Bitcoin is genuine, miners begin to verify the transaction by solving a proof-of-work problem, which is an incredibly complex math problem. The transaction is approved only after miners look into the transaction history of Hema to verify if she has enough valid Bitcoins to process the transaction. Once approved, this transaction is updated in the public ledger as a new block and the message is propagated to all the users in that blockchain network. The miner who validates the transaction first gets to place the next block into the blockchain. To incentivise mining, the miners are rewarded with newly released Bitcoins. This provides a smart way to issue the currency and also creates an incentive for more people to mine.

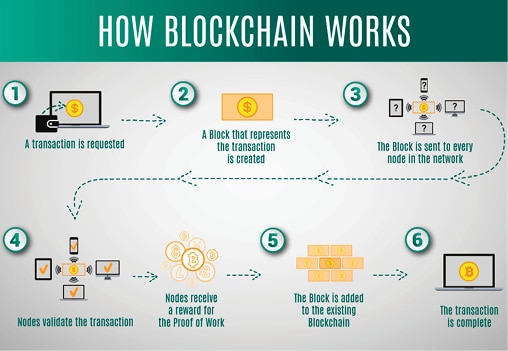

Blockchain technology – how it works

Blockchain technology is based on a decentralised, distributed ledger system. Working with blockchain can be understood based on how a new block is added to the blockchain network. The steps that are carried out during the operation in the blockchain network are depicted in Figure 2 and described below.

Step 1: Let us suppose User A wants to send 500 Bitcoins to User B. Then, A requests a transaction.

Step 2: The User A’s node starts a transaction by first creating and then digitally signing it with A’s private key (created via cryptography). A transaction can represent various actions in a blockchain.

Step 3: The transaction is propagated (flooded) by using a flooding protocol, called a gossip protocol, to peers who validate the transaction based on pre-set criteria. Usually, more than one node, called miners, can verify the transaction.

Step 4: Once the transaction is validated, it is included in a block, which is then propagated onto the network. At this point, the transaction is considered confirmed.

Step 5: The newly-created block now becomes part of the ledger and the next block links itself cryptographically back to this block. This link is a hash pointer.

Step 6: When that new block is added to the blockchain, it becomes publicly available for anyone to view. The blockchain transaction is now complete and the ledger is updated.

Blockchain and security

One of the important aspects of blockchain technology is that no one can manipulate the recorded transaction data. This is because, in the blockchain network, every transaction is propagated between nodes using a decentralised distributed ledger in a peer-to-peer (P2P) manner. In addition, an advanced level of encryption, along with the hashing mechanism (SHA-256), is used. Thus, this technology is highly secure as it is almost impossible to tamper with or hack the transactions.

The importance of open source software for blockchain technology

Open source software is collaboratively produced, shared freely, published transparently and developed for the good of the community. It is not the property of a single company or person. It ensures better transparency and offers new possibilities. Open source software provides several key benefits for blockchain projects, as listed below:

- Enables developers to build purpose-specific Bitcoin-compatible applications (e.g., a wallet app for smartphones).

- Enables the building of a new cryptocurrency that ceases to be compatible with the Bitcoin network and thereby creates new cryptocurrency networks (e.g., Litecoin or Zcash).

- Facilitates transparency by requiring new entries to include a proof-of-work.

- It enhances transparency and offers new possibilities to be tapped.

Platforms for building blockchain technology

Some of the most popular blockchain frameworks include the following.

Ethereum: This is an open source distributed cloud platform that enables developers to build and deploy decentralised applications. Ether is the built-in cryptocurrency of Ethereum that works on the public blockchain network. Ethereum is the first and the most popular smart contract platform that enables users to define smart contracts in the form of code.

Hyperledger: This is an open source, modular architecture targeted at businesses that aim to streamline their processes leveraging blockchain technology. Ethereum is an open and distributed platform on which it is impossible to hide a transaction from anyone. Hyperledger, on the other hand, offers this flexibility.

R3 Corda: This has a unique approach to data distribution, whereby the data is shared only between the authorised participants and not the entire network. Since it operates in a permission mode, it enhances privacy and offers fine-grained access control to digital records.

| Key differences between Ethereum, Hyperledger and R3 Corda | |||

| Features | Ethereum | Hyperledger | Corda |

| Governance | Ethereum developers | Linux Foundation | R3 consortium |

| Smart contract programming | Solidity | Go, Java | Kotlin, Java |

| Consensus algorithm | Proof-of-work | Pluggable framework | Pluggable framework |

| Ledger type | Permissionless | Permissioned | Permissioned |

| Currency | Powered by Ether native currency | Does not have an inbuilt native cryptocurrency. However, this can be created using chain code | Does not an have an inbuilt native cryptocurrency |

| Use cases | Popular with generalised applications and mostly used for business-to-consumer operations | Mostly used for business-to-business and enterprise applications | Preferred for financial services applications |

Industry use cases and trends of blockchain

Healthcare: Different healthcare service providers use their own database systems (private), which contain crucial information about their patients. This is scattered and inaccessible (to other providers) and is very dangerous in an industry in which even a few extra seconds taken to obtain critical information could impact a patient’s life. Blockchain makes healthcare-related data easily accessible amongst all providers, which leads to better and faster treatment.

Insurance claims: Blockchain technology can be applied to the insurance sector. Through a smart contract, customers’ and insurers’ claims can be managed in a transparent and secure manner.

Media: Media companies have started to adopt blockchain technology to eliminate fraud, reduce costs and even protect intellectual property (IP) rights on content like original music.

Energy: Another potential application of blockchain technology includes the execution of energy supply transactions to provide the basis for metering, billing and clearing processes.