The blockchain is today being used in a range of applications and fields, including e-governance, logistics and financial transactions. There are quite a few platforms and toolkits that are available today that can be used for developing a blockchain.

As per a report from GrandViewResearch.com, there is a huge scope for blockchain based implementations. Between 2022 and 2030, the market for blockchain technology is projected to increase at a compound annual growth rate (CAGR) of 85.9 per cent, from a market size of US$ 5.92 billion in 2021. Increased venture capital investment for blockchain technology startups is one of the reasons for this market expansion. For instance, blockchain technology supplier Circle Internet Financial Ltd revealed in May 2021 that it had secured US$ 440 million in investment from institutional and strategic investors. Legalisation of cryptocurrencies in nations like El Salvador and Ukraine is expected to open up new avenues for blockchain expansion.

The key applications and use cases of blockchain are:

- Cryptocurrencies and financial transactions

- Supply chain management

- Non-fungible tokens (NFTs)

- Digital health records

- Smart contracts

- E-governance

- Secured personal information

- Gaming

- Digital voting

- Internet of Things (IoT)

The blockchain market is divided into digital identity, exchanges, remittances, smart contracts, logistics management, and others based on applications. Blockchain technology increases the effectiveness of payment systems, lowers operational costs, and makes transactions transparent. Due to the advantages that it offers, its application in payment solutions is growing. Blockchain eliminates the need for a facilitator in the processing of payments, which is another important reason for its growth.

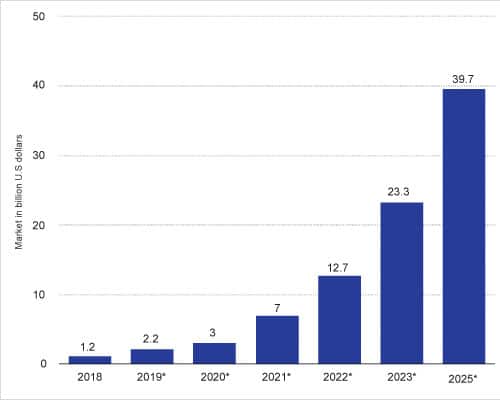

According to data from Statista.com, the market size of blockchain technology has been growing quite quickly over the past several years, and is expected to reach close to US$ 40 billion by 2025.

The acceptance of cryptocurrencies in some countries is encouraging companies and investors to increase their investments in blockchain technology. Decentralised finance (DeFi) is a new blockchain-based financial system that lessens the power banks have over financial services and payments. Market growth of blockchain technology is anticipated to be driven by strategic efforts in the decentralised finance domain.

Table 1: Frameworks, platforms and toolkits for blockchain development

| Platform and software toolkit | How it can be used in blockchain development |

| Truffle Suite URL: https://trufflesuite.com/ |

Useful for smart contracts development and blockchain emulation |

| Solidity URL: https://soliditylang.org/ |

Multi-featured programming language for smart contracts |

| Vyper URL: https://vyper.readthedocs.io/ |

Secured and contract oriented programming language |

| Rust URL: https://www.rust-lang.org/ |

Efficient and reliable software for blockchain development |

| Hardhat URL: https://hardhat.org/ |

Extensible, fast and flexible environment for blockchain development |

| Embark URL: https://framework.embarklabs.io/ |

Powerful framework for decentralised apps development |

| ThirdWeb URL: https://thirdweb.com/ |

Framework for Web3 development in the blockchain environment |

| Geth URL: https://geth.ethereum.org/ |

Implementation patterns and modules for Ethereum |

Blockchain vs traditional applications

Blockchain improves the traceability, security, trustworthiness, and transparency of data shared across a corporate network while saving costs. The traditional web based applications are centralised, which can be exploited or hacked by malicious traffic.

Blockchain for businesses employs an open, unchangeable digital ledger that only authorised blockchain members can view. The nodes of the network control what data each organisation or member may view, and what actions they may take. Because business partners don’t have to trust one another, blockchain is frequently referred to as a ‘trustless’ network.

This trust is based on the increased security, transparency, and immediate traceability of blockchain technology. Beyond issues of trust, blockchain offers commercial advantages such as cost savings due to accelerated speed, efficiency, and automation of transactions.

Blockchain technology has the potential to fundamentally alter how sensitive and important data is seen. It reduces fraud and illegal behaviour by generating a record that cannot be changed and is encrypted end-to-end. By employing permissions to restrict access and anonymizing personal data, privacy concerns are addressed. In order to prevent hackers from accessing data, information is kept across a network of computers rather than on a single server.

Without blockchain, every company needs to maintain a different database. Blockchain employs a distributed ledger, which ensures that transactions and data are recorded consistently across all locations. Full transparency is offered since any network user with permissions may see the same data at once. All transactions are time- and date-stamped records with immutability. Members may access the whole transaction history thanks to this, which almost eliminates the possibility of fraud.

Blockchain establishes an audit trail that records an asset’s origins at each stage of its travel. This helps industries plagued by fraud and counterfeiting. Blockchain makes it feasible to directly communicate provenance information to customers. Traceability data can reveal weak points in any supply chain, such as items stored on a loading dock while being transported.

Traditional paper-intensive processes take a long time, are subject to human mistakes, and frequently need third-party mediation. Transactions may be finished more quickly and effectively by automating these operations with blockchain. The blockchain can hold both documentation and transaction information, doing away with the necessity for paper exchange. Clearing and settlement happens more quickly because there is no need to reconcile several ledgers.

With smart contracts, transactions can be automated, enhancing productivity and accelerating processes even further. The subsequent stage in a transaction or workflow is automatically initiated after pre-specified requirements are met. Smart contracts lessen the need for human involvement and rely less on outside parties to confirm that a contract’s provisions have been adhered to. For instance, when a consumer files a claim for insurance, it can be immediately settled and paid once he or she has submitted all the required evidence.

Platforms and toolkits for blockchain development

A number of frameworks and programming platforms are available to develop and deploy blockchain based applications. Table 1 lists some of the important ones.

Blockchain technology has a vast array of development frameworks and platforms for use in many applications. Many of these platforms are open source and free, and can be used to design and develop algorithms in a variety of fields, such as security, authentication, privacy, and cryptocurrency.

{kind=link}