Algorithms can help automate trading decisions using financial theory, statistical modelling, and computer programming. Python has emerged as a popular language for algorithmic trading.

The use of computer algorithms to automatically carry out trading decisions in financial markets is known as algorithmic trading, or ‘algo trading’. Traders create mathematical models and rules that control when and how trades should take place rather than manually giving buy or sell orders. To find profitable trading opportunities, these algorithms examine market data, including price, volume, volatility, and other indicators.

In today’s financial markets, algorithmic trading has taken centre stage. To execute strategies quickly, accurately, and consistently, large institutional investors, hedge funds, and proprietary trading firms mainly rely on automated trading systems. The adoption of algorithmic trading has been further expedited by the quick development of computer technologies, high-speed networks, and data availability.

Python has become one of the most widely used programming languages for algorithmic trading because of its ease of use, adaptability, and plenty of libraries for financial modelling, machine learning, and data analysis.

Concept of algorithmic trading

In financial markets, algorithmic trading is the process of creating trading signals and carrying out orders automatically using pre-established rules and computing models.

An algorithmic trading model’s general structure can be expressed as:

Trading signal = f (Market data, Indicators, Model parameters)

…where:

- Market data includes price, volume, and other financial variables.

- Indicators represent derived metrics such as moving averages or momentum.

- Model parameters are predefined thresholds or coefficients.

An automatic execution engine places the order in the market after a trading signal is issued.

The entire trading pipeline may be written as:

Trade = Execution(Signal)

Algorithmic trading makes it possible to react quickly to changes in the market and lessens human emotional bias.

Typically, an algorithmic trading system is made up of several parts that collaborate to create and implement trading strategies.

Market data acquisition

Acquiring trustworthy market data is the first stage in algorithmic trading. This comprises:

- Historical pricing information

- Current market information

- Details about the order book

- Financial and economic indicators

OHLCV values are typically found in market data, where:

- O: Open

- H: High

- L: Low

- C: Close

- V: Volume

Technical analysis and quantitative modelling are based on these characteristics.

Data preprocessing

Preprocessing is required prior to analysis of financial data as raw financial data often contains missing values, irregular timestamps, or outliers.

Typical preprocessing procedures consist of:

- Managing values that are missing

- Normalisation of data and feature engineering

- Alignment of time series

For example, a moving average indicator is computed as:

….where Pt is the price at time t and n is the window length.

Signal generation

Mathematical models or predetermined rules are used to produce trading signals. These regulations could be based on:

- Technical indicators

- Models of statistics

- Algorithms for machine learning

- Models with several factors

A straightforward moving average crossover approach, for instance, produces a buy signal when:

….and a sell signal when:

![]()

This type of strategy attempts to capture market trends.

Risk management

An essential part of algorithmic trading is risk control. If risks are not well managed, even winning tactics might result in large losses. Important risk management strategies consist of:

- Stop-loss orders

- Sizing of positions

- Diversification of portfolios

- Control of maximum drawdown

The following is an example of a basic stop-loss rule:

![]()

If the loss exceeds the threshold, the position is automatically closed.

Order execution

The system uses an exchange API or brokerage interface to send orders to the market once a trading signal has been created. Algorithms for execution seek to reduce:

- Market impact

- Transaction costs

- Slippage

Examples of execution algorithms include:

- Time Weighted Average Price (TWAP)

- Volume Weighted Average Price (VWAP)

- Smart Order Routing (SOR)

Backtesting

Backtesting uses past market data to assess a trading strategy’s performance. Before implementing techniques in actual markets, it enables traders to assess possible risks and rewards.

Key performance indicators consist of:

- Total return

- Sharpe ratio

- Maximum drawdown

- Win-loss ratio

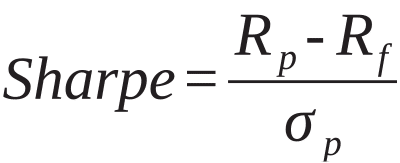

The definition of the Sharpe ratio is:

…where:

Rp= Portfolio return

Rf= Risk-free rate

óp= Standard deviation of portfolio returns

Applications of algorithmic trading

Algorithmic trading is used in several trading strategies.

Trend-following: The goal of trend-following tactics is to record long-term price changes.

Examples of indications are:

- Moving averages

- Moving Average Convergence Divergence, (MACD)

- Trend lines

MACD gauges momentum; ‘convergence’ happens when moving averages go closer together, and ‘divergence’ happens when they get further apart.

Mean reversion: Price variations between related markets or instruments are exploited by arbitrage methods.

Examples are:

- Statistical arbitrage

- Pair trading

- Index arbitrage

High-frequency trading: In high-frequency trading (HFT), a lot of orders are executed in incredibly short amounts of time. These tactics mostly depend on:

- Ultra-low latency systems

- High-speed data processing

- Advanced algorithms

Advantages of algorithmic trading

Compared to manual trading, algorithmic trading has several advantages.

Faster: Algorithms can process market data and complete trades in milliseconds.

Accurate: Order placement errors are eliminated by automated processes.

Discipline: Rather than being influenced by feelings, trading decisions are based on predetermined rules.

Capability of backtesting: Before being implemented, strategies can be tested on past data.

Limitations and risks

However, algorithmic trading also has certain drawbacks.

Model risk: If the market conditions shift, trading tactics cannot work.

Overfitting: Although it may do well on historical data, it may perform poorly in the real market.

Technology risks: Trading losses may result from connectivity problems or system malfunctions.

Market effects: Large orders could lower profitability and affect market prices.

Data sources for algorithmic trading

A number of online data sources and application programming interfaces (APIs) provide timely and accurate financial market data, which is essential for algorithmic trading. Yahoo Finance, which offers free historical market data for equities, indexes, exchange-traded funds, and cryptocurrencies, is one popular source. Python tools like yfinance and pandas-datareader are frequently used by traders and researchers to access this data, making it useful for backtesting and strategy building. The National Stock Exchange of India, which offers official information on stock prices, indexes, derivatives, and trading volumes, is another source of data on the Indian market. To access real-time and historical market data directly within trading algorithms, many algorithmic traders also make use of APIs provided by brokers and data providers, such as Alpha Vantage, Quandl, or brokerage platforms. These APIs enable continuous data retrieval, trading algorithm processing, and trading signal generation by automated systems. Thus, one of the most important steps in creating strong algorithmic trading systems is choosing suitable and trustworthy data sources.

Algorithmic trading: What one should learn

Successful algorithmic trading integrates programming, mathematics, and trading expertise into a cohesive framework.

This can be summed up as follows:

- Trading knowledge identifies market opportunities.

- Mathematics and statistics develop predictive models.

- Programming languages implement and automate the strategy.

This relationship can be expressed as:

Algorithmic trading = Market knowledge + Mathematical model + Computational impleementation

Algorithmic trading is a multidisciplinary field requiring knowledge of financial markets, quantitative analysis, and computer programming. A trader should understand market dynamics, use mathematical models to assess financial data, and implement strategies in programming languages such as Python. By merging these three areas, traders can create automated systems capable of analysing massive amounts of market data and effectively executing transactions. Developing trading, mathematics, and programming skills serves as the foundation for becoming a great algorithmic trader.

Mathematics and statistics

Mathematics is essential in algorithmic trading since trading methods frequently rely on quantitative models and statistical analysis.

Probability theory: Probability is useful in evaluating uncertain market outcomes. The probability of positive returns can be represented as:

P(Return>0)

Trading techniques generally target scenarios with a high probability.

Statistics: Statistical methods are used to analyse financial time-series data. Important statistical concepts include:

- Mean and variance

- Correlation

- Regression analysis

- Hypothesis testing

- Time-series modelling

For example, the expected return of a portfolio can be calculated as:

…where wi represents asset weights and Ri represents returns.

Linear algebra: Linear algebra is used in machine learning models and portfolio optimisation. The key subjects include:

- Vectors and matrices

- Eigenvalues and eigenvectors

- Matrix multiplication

- Principal component analysis

Optimisation: Optimisation approaches help in determining the most effective trading settings or portfolio allocations. An example portfolio optimisation target is:

subject to risk constraints.

Why Python is popular

Python is the most popular language for algorithmic trading due to its ease of use and robust data analysis packages. Python syntax is simple to learn and understand, making it appropriate for both programmers and financial analysts.

Python has a robust ecosystem of libraries for financial analysis and machine learning:

| Library | Purpose |

| NumPy | Numerical computation |

| Pandas | Data analysis |

| Matplotlib | Data visualisation |

| Scikit-learn | Machine learning |

| TensorFlow | Deep learning |

| TA-Lib | Technical indicators |

Python is commonly used for data analysis, strategy development, backtesting and machine learning models. It excels at working with massive datasets and executing advanced statistical analyses. Pandas data structures such as DataFrames, for example, make it simple to manipulate financial time series data. This feature is very beneficial for evaluating high-frequency market data.

Integration with machine learning

Machine learning models are increasingly being utilised in algorithmic trading to forecast market movements and uncover hidden patterns in financial information.

Examples of machine learning approaches in trading include:

- Linear regression

- Random Forest

- Gradient boosting

- Neural networks

- Reinforcement learning

A typical predictive model can be represented as:

…where Xi are explanatory variables or market features.

R is widely used in statistical analysis and quantitative finance. It is particularly useful for:

- Statistical modelling

- Financial econometrics

- Time-series analysis

C++ and Java are frequently used in high-frequency trading systems because they provide quicker execution rates and lower latency. These languages are commonly used for:

- Real-time trading systems

- Low-latency order execution

- High-frequency trading infrastructure

As technology and data science develop, so will algorithmic trading. Key future trends include:

- Artificial intelligence in trading

- Alternative data analysis

- Reinforcement learning trading agents

- Cloud-based trading infrastructure

These advances will improve the capability of automated trading systems.

With financial markets creating vast volumes of data, machine learning, big data analytics, and high-performance computers will become increasingly vital in algorithmic trading. Hence, financial analysts, quantitative researchers, and traders will need to understand algorithmic trading principles and grasp languages like Python.

{kind=link}